There are no required payments on a reverse mortgage—this type of mortgage accretes, unlike a typical amortizing mortgage that amortizes. Hence, mathematically, instead of an amortization schedule associated with an amortizing mortgage, you end up with a reverse amortization schedule and a mortgage where the outstanding balance accretes or grows. The homeowner is still responsible for paying the property taxes and insurance.

Hence, if you swap out an amortizing mortgage for a reverse mortgage, you will eliminate your monthly mortgage payment (from a monthly cash flow perspective only) but not your real estate taxes or homeowners insurance. You will still owe the accrued interest despite not having to make monthly mortgage payments. Instead, the monthly interest is deferred, meaning it is not paid immediately, and added to the mortgage's outstanding balance. This can lead to a significant increase in the total amount owed over time. This elimination and deferment of monthly mortgage payments is why the income requirements for obtaining a reverse mortgage are less stringent than those for an amortizing mortgage. On a reverse mortgage, the borrower will still have to show enough income or alternative assets to cover the real estate taxes and insurance.

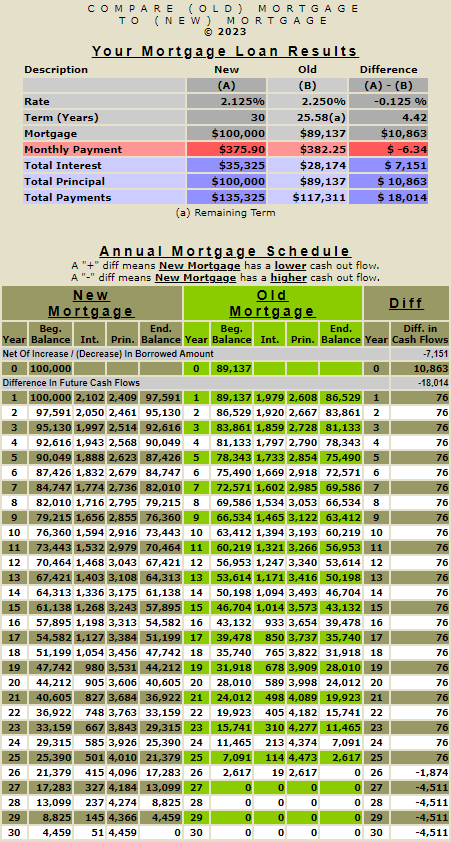

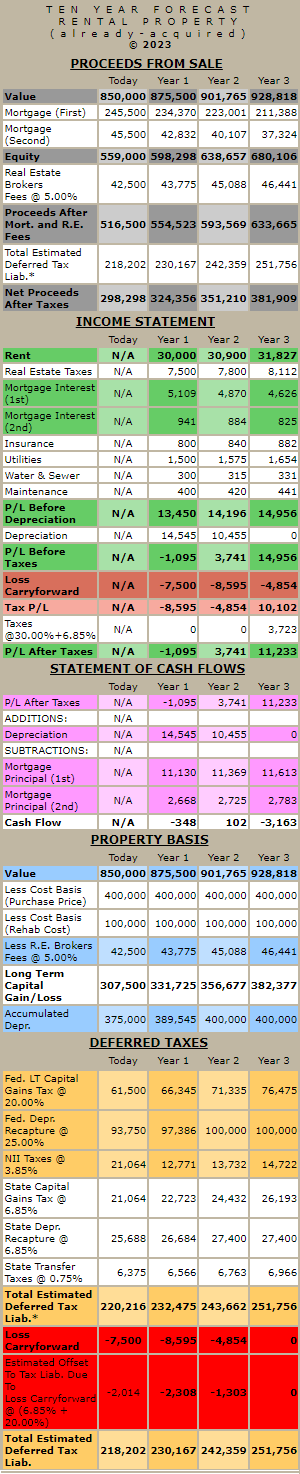

Continue on the following page to compare the accumulative numeric results of an amortizing mortgage versus a reverse amortizing mortgage (reverse mortgage).